》Check SMM aluminum product quotes, data, and market analysis

》Subscribe to view historical spot prices of SMM metals

Aluminum billet inventory

- According to SMM statistics, as of June 26, the inventory of aluminum billets in major domestic consumption areas stood at 142,500 mt, a decrease of 2,000 mt from Monday and an increase of 8,000 mt compared to last Thursday. The inventory trajectory indicates that the inflection point of aluminum billet inventory has been basically confirmed, and the inventory has moved away from the low levels of the same period in the past three years, with the advantage of low inventory gradually diminishing. Regionally, there are differences in the situation. In Wuxi, due to an increase in truck shipments and a trend of reduced aluminum billet production at aluminum plants, there has been less inflow of goods. In Nanchang, due to price spread advantages, there are still many arrivals. In South China, while the volume of arrivals remains stable, downstream consumption is weak, leading to a continued rise in inventory.

- In terms of aluminum billet consumption, according to SMM statistics, the total outflows from warehouses of domestic aluminum billets during the period from June 17 to June 22 were 35,800 mt, a decrease of 2,400 mt from the previous period, reflecting the weak market transaction performance of aluminum billets. Despite entering the off-season for market consumption, aluminum billet manufacturers will further consider production cuts due to cost and order expectations, and subsequent arrivals of aluminum billets may be affected by supply-side disruptions. According to SMM surveys, aluminum billet manufacturers in Shandong, Guangxi, Qinghai, and Yunnan have already taken marginal production reduction measures, and the pressure on the supply side of the aluminum billet market is expected to ease. In addition, as of June 27, 2025, SMM recorded an in-plant inventory of 113,700 mt for primary aluminum billet plants, an increase of 6,000 mt MoM, indicating that aluminum billet manufacturers are gradually facing order pressure and the market is gradually moving away from a balanced state of production and sales.

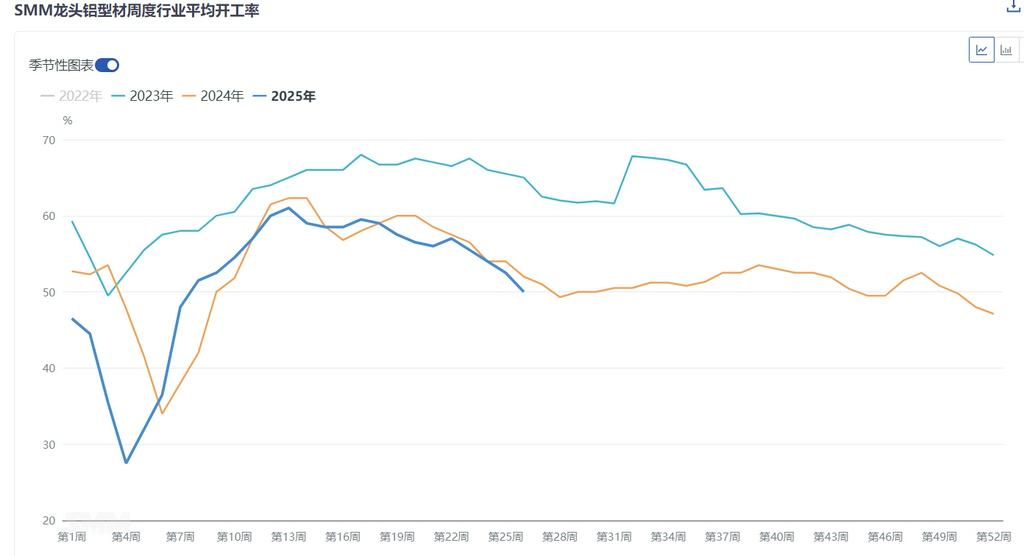

Extrusions

- In the past week, the national operating rate of extrusions dropped slightly by 2.5 percentage points MoM to 50.0%. In the construction materials sector, the overall operating rate of sample enterprises declined compared to last week. According to SMM surveys, top-tier enterprises in central China, South China, and east China all reported sluggish growth in new orders this week, only maintaining production of orders on hand, leading to a decline in the operating rate. Some small and medium-sized construction extrusion enterprises in Shandong reported that despite the decline in aluminum prices this week, their customers still had a strong wait-and-see sentiment, and they reported that downstream customers tend to believe that the earlier they place orders when prices are expected to fall, the more likely they are to place orders at a high point, with customers generally preferring to place orders when prices are expected to bottom out.

- This week, the operating rate of industrial extrusions dropped slightly compared to last week. PV frame sample enterprises reported that they are negotiating next month's cooperation with module factories. Some top-tier PV frame extrusion enterprises in east China, southwest China, and Hebei reported that orders for next month are expected to decline, and this week's production orders cannot be linked with next month's orders. Additionally, some processing enterprises expect that the processing fee for PV frames may further decline, compressing corporate profitability and leading to a drop in the operating rate.

- In terms of automotive extrusion, some large and medium-sized sample enterprises in east China and central China reported that due to the obstruction of destocking at some OEM plants and the slowdown in production speed, new orders were weak. Coupled with insufficient orders on hand, their operating rates dropped to around 50%. Despite active negotiations for new cooperation, relevant enterprises had not yet implemented them. Other industrial extrusion producers, such as those in rail transit and power pipelines, maintained operating rates basically unchanged from the previous week this week. The main reason was that their orders were mainly long-term contracts from long-established customers, with a relatively stable customer base. Overall, influenced by the off-season in consumption, the overall operating rate of aluminum extrusion declined significantly. SMM will continue to monitor the actual implementation progress of orders in various fields.

Outlook

- SMM believes that in the short term, aluminum ingot inventory will remain below 500,000 mt, and high aluminum prices will continue to fluctuate at highs, suppressing downstream consumption. After experiencing short-term consumption-stimulating phases such as "installation rush" in the PV sector and "export rush", downstream extrusion orders are weakening. Coupled with seasonal influences, extrusion producers' order expectations are weak, and they maintain a wait-and-see attitude towards raw material purchases, leading to weak destocking and a clear establishment of the inventory buildup turning point for aluminum billet. Despite reports of reduction measures by aluminum billet producers in the market over the past week, due to the increased proportion of road transportation in the market and the initial stage of in-plant inventory accumulation, there may be a certain time lag before the off-season sentiment in the downstream sector is transmitted to an increase in visible social inventory. Therefore, although the inventory buildup turning point for aluminum billet has been established, influenced by changes in the aluminum billet supply side, the growth trend may remain mainly slow. It is expected that aluminum billet inventory will remain within the range of 135,000-160,000 mt in the short term, and the production cut rhythm of aluminum billet producers in various regions will still need to be monitored subsequently.